Wheel Strategy: A Long-Term Strategy For Consistent Income

The wheel strategy (a.k.a "options wheel strategy") is a two-step "Buy Low-Sell High" income strategy used by stock options traders who sell cash-secured puts and covered calls in order to receive stock at a discount, and then sell at an above-market price. With just a few small adjustments, crypto traders can also benefit from this strategy.

Step 1:

An investor continually sells (writes) Out-of-The-Money (OTM) cash-secured puts to collect option premium.

If at the predetermined expiration date the option expires worthless, the writer keeps all the premium — repeating the process until a put eventually expires In-The-Money (ITM).

A put option expiring in-the-money (ITM) exercises automatically.

Unlike traditional equity options where a physical transfer of ownership takes place when exercising an option contract — Bybit's USDC crypto options are "cash-settled". Here, no position transfer takes place. Instead, the option seller's account is credited or debited to the associated cash (USDC) position.

Example:

The investor sells one BTC $20,000 put option and receives a $2,000 premium from the buyer.

The option contract expires at a settlement price of $19,000 and the seller's account receives a credit of +$1,000 USDC (Strike Price - Settlement Price + Premium Received)

At this point, the option seller enters the market and purchases one BTC, before moving to step 2 of the wheel strategy.

Step 2:

Now holding the underlying crypto asset, the investor sells out-of-the-money (covered) calls to generate a consistent income.

When a call option eventually expires in-the-money — there are two available options:

Option 1: Sell the underlying crypto asset and return to Step 1 selling cash secured puts.

Option 2: Keep the underlying asset and continue selling covered calls to generate income.

Wheel Strategy Setup

The most important factor when using the wheel strategy is ensuring your trading account has enough capital to cover the difference between the strike price and the settlement price if the option expires in-the-money. Here, the account balance guarantees the short put is "cash-secured".

Selling a put option is a high-risk strategy with limited upside (collected premium) and significant potential downside — the difference between the strike price and the settlement price, minus the premium received.

For this reason, the chosen strike price should represent a level you are happy to open a long-term position in the underlying asset.

Choosing Which Put to Sell:

When deciding which put option to sell, there are two main considerations:

How far out-of-the-money (below the current market price) should the strike price be to achieve the desired result (either expiring worthless or being exercised)?

How many Days-To-Expiration (DTE) should the option have?

If the goal is for the option to expire worthless (collect premium), selling a put with a strike price way below the current market price works better - the lower the strike price, the less chance the option will expire in-the-money. The trade-off is that option premiums decrease the further out-of-the money you go.

If the aim is acquiring the underlying crypto asset, choose a higher strike price you believe will expire in-the-money — ideally not by too much as to offset the amount of premium received.

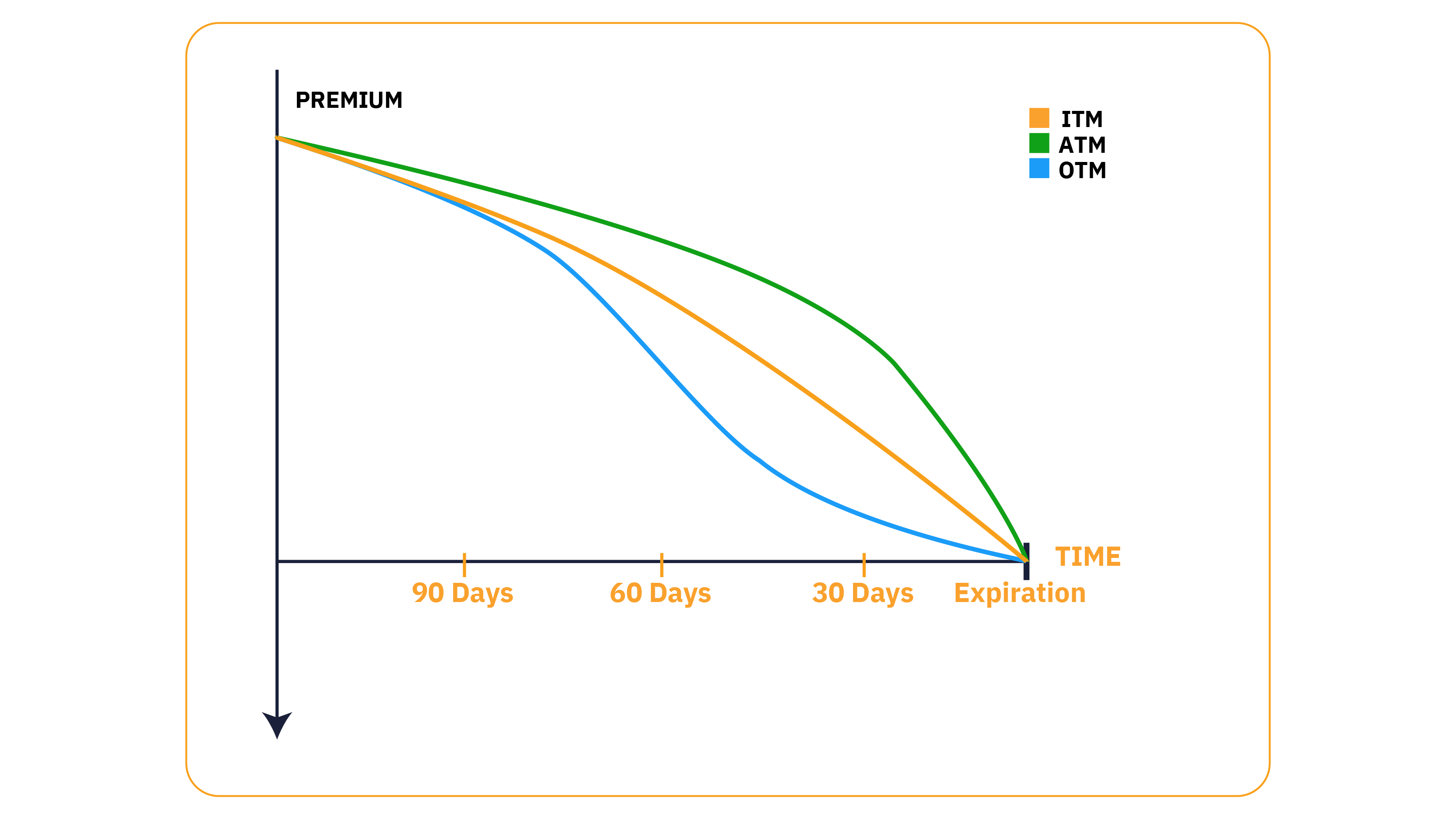

Before deciding which maturity (expiration date) to sell, consider how the option premium changes over time. All options lose value (time decay) as the expiration date draws near. We can measure exactly how much value an option will lose by using Theta.

Theta is an options Greek measuring the rate an option premium declines over time - as an option moves closer to expiry, time decay speeds up — at expiration the option has zero time value.

A handy way to visualize theta is to imagine a snowball rolling down a mountain. At the top of the mountain, the snowball is small and moving slowly. As it rolls further down the mountain, it speeds up, growing larger along the way, until it reaches the bottom (expiration).

An option with a theta of -0.50 will lose $0.50 each day whereas an option with a theta of -2.00 will lose $2.00 per day. Theta is always represented as negative as it always has a negative effect on an option's price.

Theta is lower for longer-dated options (price decays less) and higher for near-dated options (price decays more).

Theta is highest for At-The-Money (ATM) options (the strike price is equal to the current price of the underlying asset) decreasing when a strike price moves further into-the-money or out-of-the-money.

For best results, selling near-dated puts with between 30-40 (DTE) offers a good way to maximize time decay whilst not being tied to a less flexible longer-term contract.

Choosing which Call to Sell:

In the same way the account balance "secures" the short put, the underlying asset provides the "cover" for the short call. For this reason, you must hold the underlying crypto asset while the short call contract is active.

When choosing which strike price to sell, consider the same factors used to determine which put to sell:

How far out-of-the-money (above the current market price) should the strike price be to achieve the desired result (either expiring worthless or being exercised)?

How many days-to-expiry should the option have?

Similar to the put, selling a near-dated call option with between 30-40 DTE offers a good mix of value and flexibility.

Wheel Strategy

Another useful metric to help decide which strike prices will work best when using the wheel options strategy is Delta.

Delta is the amount an option premium changes for every $1.0o change in the underlying asset. Call options have a positive delta ranging between 0 and 1 - whereas put options carry a negative delta ranging between -1 and 0.

For call options, the delta tells us how much the price will rise when the underlying asset ticks higher by $1.00 and how much the price will drop when the underlying asset drops by $1.00. This works in reverse for put options, which lose value when the underlying asset rises, and gain when the underlying assets fall.

Typically, an at-the-money call option will have a delta of - or close to 0.50, meaning the premium will +/- $0.50 for every $1.00 move in the underlying price.

Delta decreases as a call option moves further out-of-the-money (higher than the current market price), and increases when a call option moves deeper into-the-money (lower) — the opposite is true for put options.

Delta is simply the options markets' way of telling us the odds of a strike price expiring in-the-money.

All things equal, an at-the-money option has a 50% chance of expiring in-the-money, and thus is a 50/50 bet - whereas a 0.20/-0.20 delta has a 20% chance of expiring in-the-money.

Higher Delta = Higher chance of expiring ITM.

Lower Delta= Lower chance of expiring ITM.

Whom the Wheel Strategy is For

The wheel option strategy is suitable for investors with a good working knowledge of options trading.

Because crypto options are cash-settled, traders must always remember to acquire the underlying asset when a short put expires in-the-money and sell (if that's the aim) when a short call expires in-the-money. For this reason, the wheel option strategy is best suited to more experienced options traders.

When to Use the Wheel Strategy

Sideways trending markets with wide trading ranges and clearly defined support and resistance levels (round numbers are often best) works great for the wheel strategy, giving you several ways to yield positive returns:

Generate passive income (when the options expire worthless).

Lower the cost basis of acquiring an underlying crypto asset (short puts expire ITM).

Increasing the net sale price of the underlying asset (short call expires ITM)

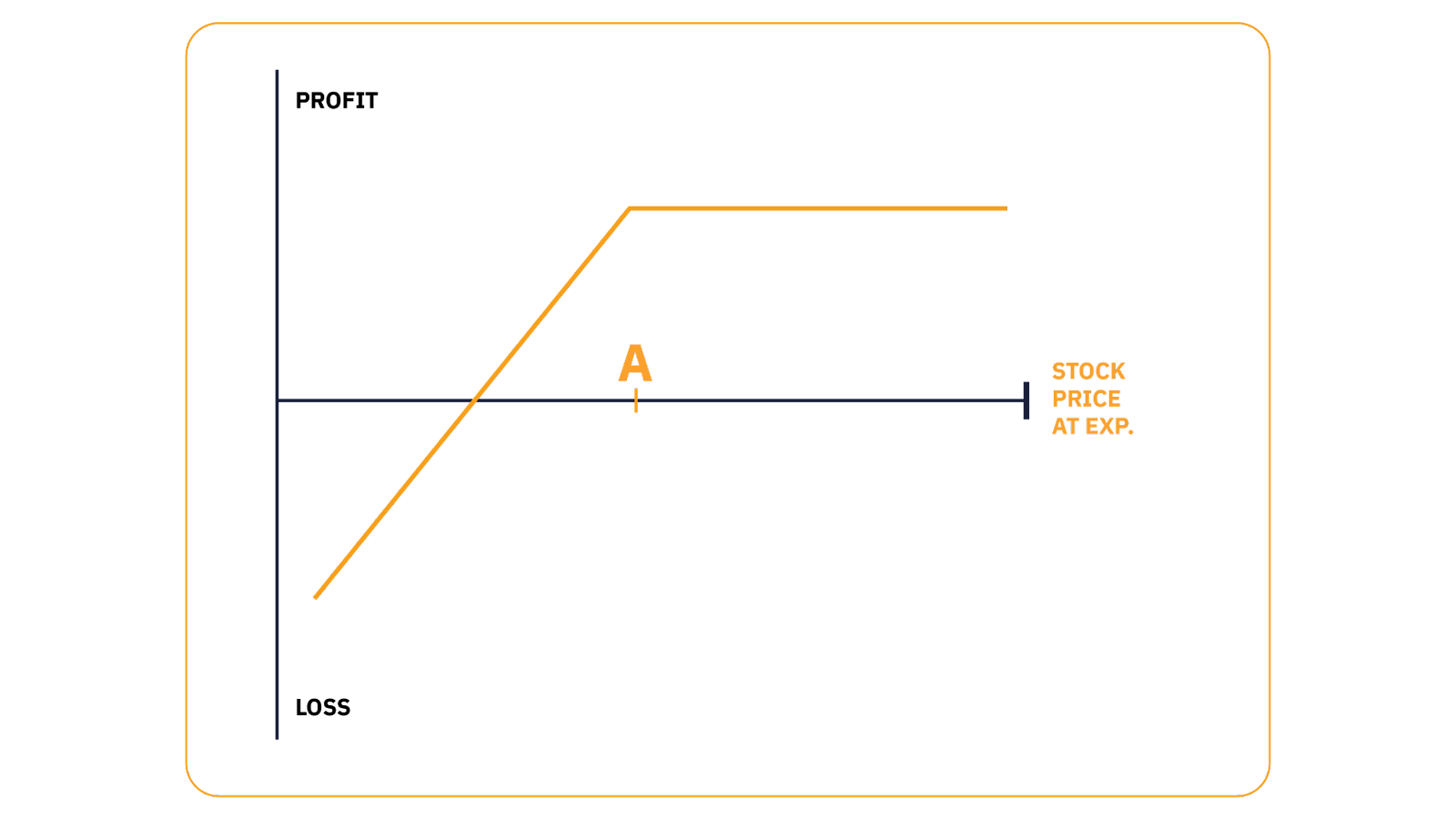

The below chart shows how you can profit from the wheel strategy:

Breakeven Point

The breakeven point is the price at which an options strategy is neither making nor losing money. Because the wheel strategy has lots of moving parts, we can't pinpoint a specific breakeven point - instead, we must look at each individual component to work out their respective breakeven points.

Cash Secured Put - Breakeven Point

The breakeven point when selling a cash-secured put is when it expires in-the-money (below the strike price) equal to the amount of premium received.

For instance:

The investor sells one BTC $20,000 put option, receiving a premium of $2,000 from the buyer.

Here, the breakeven for the put writer is $18,000. If the put expires at $18,000 their account is debited -$2,000 (Strike price - Settlement Price) and receives a credit of $2,000 (Premium Received)

Because the wheel strategy involves acquiring an underlying asset and then selling calls against it, we must also factor in the price of acquiring the underlying asset into our calculation.

Typically, the option seller buys the underlying crypto asset when the put option expires. Choosing not to can impact profitability in three ways:

Neutral Outcome

The writer purchases the underlying asset at the same level as the settlement price:

Settlement Price of $18,000 - Purchase Price of $18,000 - no change

Positive Outcome

The option writer purchases the underlying asset below the settlement price:

Settlement price of $18,000 - Purchase price $16,000 — a saving of $2,000.

Negative Outcome

The writer purchases the underlying asset above the settlement price:

Settlement Price of $18,000 - Purchase Price of $20,000 — a loss of $2,000.

Note: To reduce risk you should purchase the underlying asset immediately if the short put option expires ITM.

Covered Call - Breakeven Point

We can work out the breakeven point for a covered call by calculating at which point the premium no longer offsets a drop in the underlying asset when the option expires.

Assuming an investor acquires one BTC at $20,000, then sells an out-of-the money call option, collecting a $2,000 premium, the breakeven point is $18,000. Here, the $2,000 premium offsets the $2000 drop in the underlying asset.

Wheel Strategy Sweet Spot

The sweet spot of an options strategy refers to the optimal price at the expiration date. Just as a wheel options strategy has more than one breakeven point, it also has several sweet spots:

Cash-Secured Put Sweet Spot

When selling a cash-secured put, the ideal settlement price is when the underlying is equal to the strike price. Here, the option expires worthless and the seller keeps the premium.

Covered Call Sweet Spot

Similar to the cash-secured put, the sweet spot for a short covered call is when the option expires at-the-money (expires worthless). The seller keeps the premium, and assuming the call was out-of-the-money when sold, the value of the underlying asset will be higher.

Adjustments to Make in Bearish Markets

One of the main advantages of trading options is their flexibility. Unlike trading spot or perpetual futures where the only choice is whether to keep the position open or close it, options traders have several ways to adjust their position during adverse market conditions.

Let's assume BTC is trading at $22,000 and an investor sells one BTC $20,000 put option with 40 days-to-expiry and receives a $2,000 premium, believing the price will be close to $20,000 at expiry.

Half way through the contract, now with 20 days-to-expiry, the investor becomes more bearish, believing BTC may trade down to $18,000 before the option's expiration date.

The underlying price has dropped $500 to $21,500 and the option premium is still $2,000 (the time-decay has offset the negative price movement of the underlying).

Here are some ways they can adjust the position to reflect their new, more bearish outlook:

Close the position and wait to sell a lower strike — If the short put is closed and BTC slides towards $18,000 before the expiration date, the investor can sell a lower strike price with a similar amount of time to run, lowering their breakeven price whilst receiving an amount of premium equivalent to that collected when writing the $20,000 put.

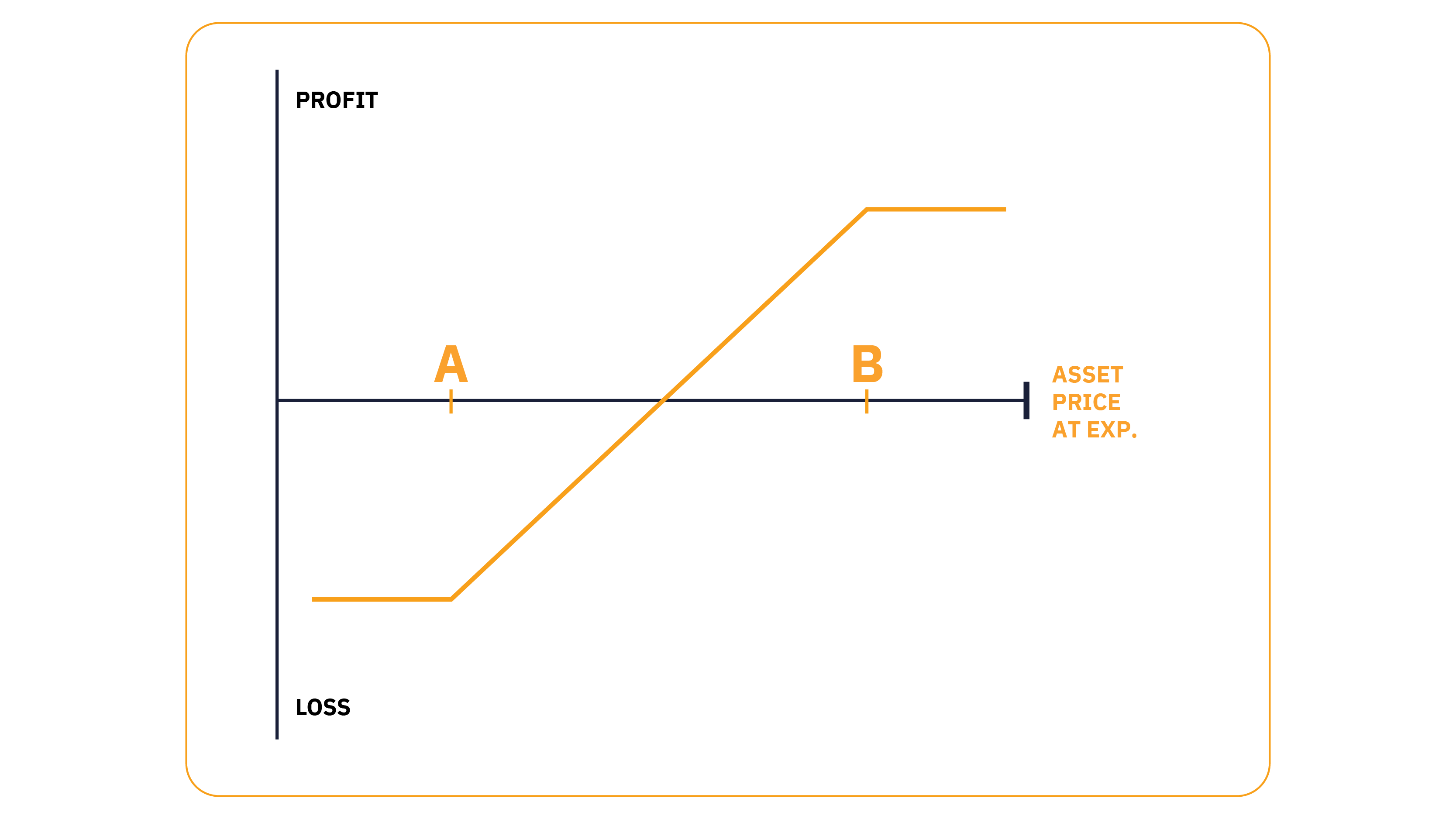

Buy a protective put option at a lower strike price - Buying a further out-of-the-money put transforms the cash-secured short put into a lower risk Bull Put Spread. The protective long put caps the amount you can lose from the short put, and because the strike is lower, it will cost less than the premium collected on the written short put. The payoff diagram for the Bull Put Spread shows it limits the potential loss, no matter how far the in-the-money the lower put expires.

Rolling Down: Rolling down involves closing an open short strike and opening a new short position in a further out-of-the-money strike in its place. Rolling up is the opposite and involves closing an open strike and opening a higher one. In this example, the investor buys back the $20,000 put and sells a strike closer to $18,000. Of course, being further out-of-the-money, the new strike will generate less premium and have lower theta — the benefit here is that the new strike has lower delta and thus is less likely to expire in-the-money.

Maximum Take Profit Potential

Because the wheel strategy is multi-faceted, in theory, there are several ways for it to play out at maximum profitably:

The short puts rarely, or never expire in-the-money, and the option writer generates a steady and reliable income.

A short put expires at-the-money (worthless) - the writer keeps the premium, buys the underlying crypto asset which duly rallies, and the investor writes covered calls to generate additional income. Here, the investor profits from the capital appreciation of the underlying asset and the received premiums.

Once holding the underlying asset, it trends higher and the investor continually writes covered calls which rarely, or never expire in-the-money.

Maximum Incurred Loss Potential

To understand the potential losses when trading the wheel strategy, we need to break it down into two parts:

Cash Secured Put

The maximum incurred loss potential is the difference between the strike price and the settlement price + premium received, In theory, the maximum loss occurs if the underlying asset price falls to $0.00. In the example we used above, the maximum loss on the short $20,000 put option is -$18,000 (-$20,000 + premium received of $2,000).

We can avoid the maximum potential loss by closing the position if either the premium or the underlying asset crosses a predetermined price threshold.

Covered call

The maximum loss on the covered call strategy is the difference between the price of acquiring the underlying asset and $0.00 + Premium received.

For instance, if an investor acquired BTC at $20,000 and sold an out-of-the-money call option receiving a $2,000 premium, the maximum potential loss is -$18,000 (-$20,000 + Premium received of $2,000).

To avoid the maximum potential loss on a covered call, the best practice is to place a stop-loss order against the underlying asset, and if filled, immediately close the short call option position.

Wheel Strategy Example

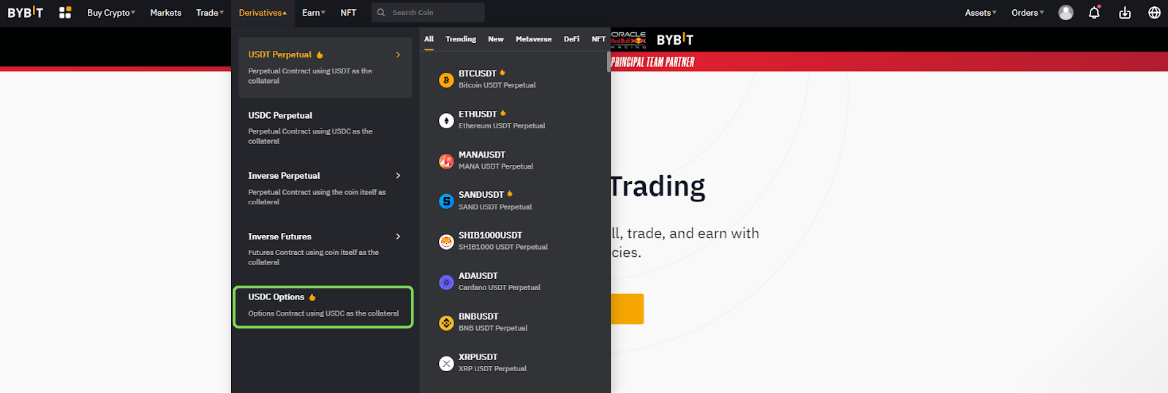

let's run through the different steps of trading wheel strategy options when using Bybit's USDC settled contracts.

Step 1

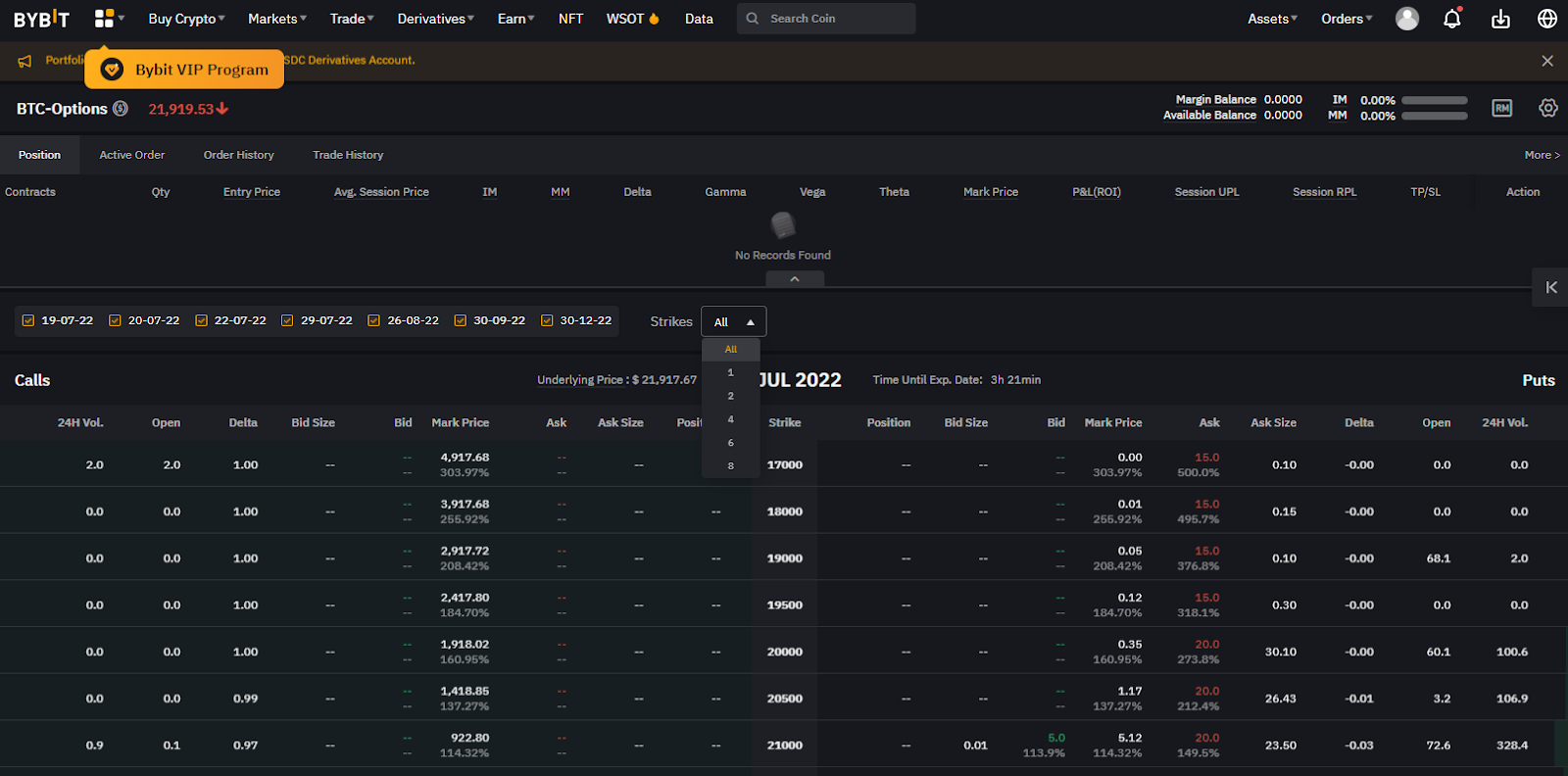

Under the derivatives tab, select USDC Options.

Step 2

Select which expiration date you wish to view — or view all the expiration dates at the same time.

Step 3

Select the desired strike price. Call options are displayed on the left of the options chain and put options on the right.

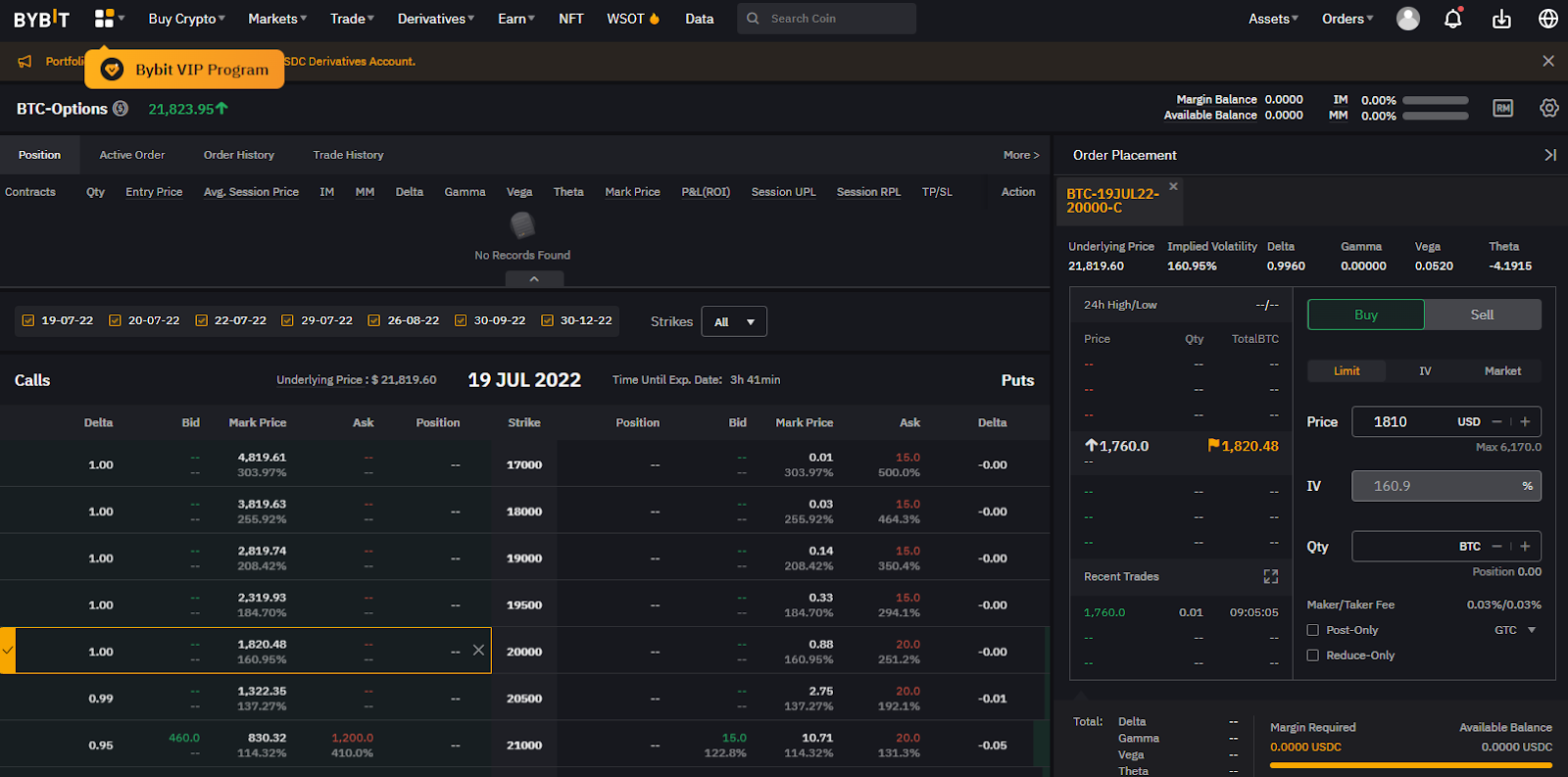

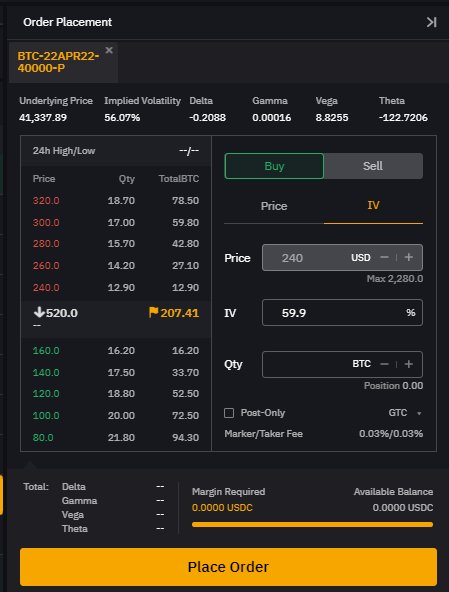

Step 4

After selecting the desired strike, an order placement ticket appears. Here you will find the implied volatility, delta, gamma and theta calculations for the strike. Once happy to proceed, click place order.

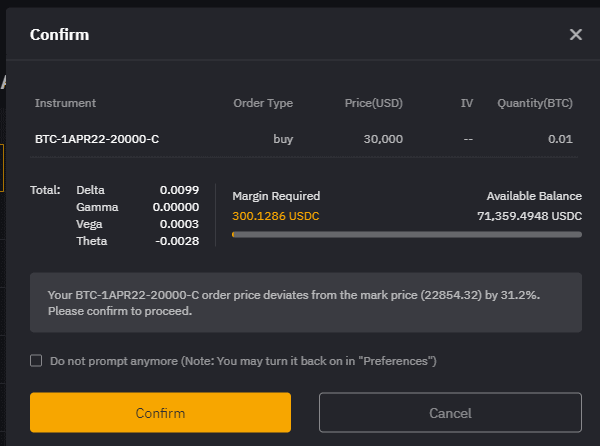

Step 5

You'll be asked to confirm the order. If everything checks out, click confirm.

Wheel Strategy Returns

The results from the trading the wheel strategy will vary depending on several things:

The total amount of premium collected (options expire worthless), before an option eventually expires in-the-money — The more premium you collect over time, the greater the chance of success.

Predicting trend reversal points in the underlying price — The aim is to "buy low and sell high." Selling puts towards the range lows and calls towards the high will improve profitability dramatically.

Timing implied volatility — Sell options when implied volatility is high by historical standards.

By understanding these three fundamental factors, you can enhance the potential profitability when trading the options wheel.

Wheel Strategy Tips

There are a few things you can do to get the best results from the wheel strategy:

Sell put/call options at a strike price you believe will expire at-the-money.

Sell options when implied volatility is high relative to the historical volatility

Write options with between 30-40 days to expiration to take advantage of time decay.

Set up alerts to notify you when an option is about to expire.

Margin Requirements

The main goal of the options wheel strategy is to gain the underlying asset in order to write call options against it. For this reason, you should maintain a USDC balance high enough to cover the cost of buying the underlying asset.

Once the underlying is acquired, account holders with a minimum account balance of 1,000 USDC can use Bybit's Portfolio Margin mode to reduce the margin requirements when selling covered call options.

Portfolio Margin mode combines the positions to determine the portfolio's overall exposure. Here, the long exposure (long underlying) will net off against the short exposure (short call), resulting in a lower combined margin requirement than if holding the positions individually. The main advantage of Portfolio Margin mode is it requires less capital to manage a hedged portfolio, increasing the buying power of the account capital.

Theta Decay Impact

Theta decay compliments the wheel options play by reducing the value of written options - especially as expiration draws near. By selling short-dated options with between 30-40 days to expiration you benefit by exploiting the steepest part of the curve where the premium decays the fastest.

Implied Volatility Effect

Volatility measures how much, and how fast an asset price moves up or down over a given period. Markets with small day-to-day price swings are low-volatility and markets with bigger day-to-day price swings are high volatility. The key difference is the high-volatility stock has much bigger price swings along the way. This is usually accompanied by a high IV.

When trading options, we express volatility in two different ways:

Historical Volatility

As the name suggests, this tells us how much the price of an asset moved on a day-to-day basis over a particular period.

Implied Volatility

Implied Volatility (IV) is the measure of how volatile the options market expects the underlying asset to be in the future.

All things being equal, the price of options rise when IV increases and falls when it decreases.

Understanding the relationship between historical volatility and IV is a great tool to have in your belt when selling options. Here, you can assess whether IV is high or low by historical standards.

To maximize profits, a good rule is to sell options when IV is high compared to its historical average. By doing this, you will command higher premiums and benefits if IV reverts to the historical mean.

Benefits

Here are some advantages of the wheel strategy:

Investors can earn a passive income by selling options and collecting premiums.

The received premiums effectively lower the purchase price and increase the sale price of the underlying asset.

Time decay works in favor of this strategy.

Cons

Here are some cons of the strategy:

Both the cash-secured put and the covered call have limited upside potential and significant downside potential.

Rising implied volatility works against this strategy.

Cash settlement means investors must make additional transactions (buying or selling the underlying asset) when employing this strategy.

Risks

The short put option expires in-the-money (exercised) and the underlying asset price jumps higher by an amount greater than the premium received before the investor executes their buy order.

The covered call expires in-the-money by more than the received premium and is exercised at a net loss. Believing the underlying will continue higher, the investor chooses not to sell, but the market turns lower resulting in a mark-to-market loss.

Wheel Strategy vs. Covered Calls

If an investor already holds an underlying crypto asset, they may skip step 1 (writing cash-secured puts) of the wheel strategy and jump straight to selling covered calls (step 2). In the event a call option is exercised, the investor may choose to sell the underlying crypto asset and begin the wheel strategy from step 1.

Wheel Strategy vs. Buy And Hold

When executed correctly, the options wheel can yield better returns than a traditional buy-and-hold strategy. Though sometimes, simply HODLing may be more profitable.

One of the deciding factors is how much option premium the writer will collect.

It's possible that writing options with 30-40 days till expiration may not result in a strike expiring in-the-money for several months. Here, the banked premiums could be considerable and used to finance the purchase price of the underlying asset, thereby achieving a better cost basis. This is clearly a positive for the wheel strategy, however, it doesn't account for lost opportunity.

Although selling put options is profitable if the market moves higher (the put expires worthless and you keep the premium), it limits the potential profit to the amount of premium received. If you believe the price of the underlying could go up more than the amount of premium you will receive for selling a put option, buying the asset outright makes more sense.

Similarly, selling calls against your underlying crypto works well when the market is trending sideways, or slightly lower. Here, the premiums provide an income stream and hedge against minor declines in the underlying crypto asset. But in a rising market, you're better off not selling calls as you could miss out if your crypto has a bullish run higher.

Wheel Strategy vs. Credit Spread

To understand the difference between the wheel strategy and credit spreads, let's look at how credit spreads work:

A credit spread is a two-legged options strategy where an investor sells one option and buys a further out-of-the-money option in the same underlying with the same expiration date. The credit spread gets its name because the short option is always closer to the money than the long option and subsequently has a higher premium - for instance:

Investor sells one BTC $20,000 put option with 40 DTE and receives a $2,000 premium

The investor buys one BTC $18,000 put option with 40 DTE and pays an $800 premium.

Here we see the investor receives a net credit of $1,200 (Premium Received of $2,000 -Premium Paid of $800)

The main difference between short options used in the wheel strategy, and a credit spread, is that buying the further out-of-the-money strike, limits the potential loss to the difference between the strike prices, minus the premium received.

When only selling the $20,000 put option, the maximum downside is $18,000 (-$20,000 +$2,000 premium received) and a maximum potential profit of $2,000 (Premium received).

Although trading the above credit spread only generates $1,200 of net premium vs. $2,000 when trading the put alone, the most you can lose is $800 ($20,000 - $18,000 + Premium received of $1,200).

Alternative Strategies

Because the short option elements of the wheel have limited upside and significant risk, the strategy may not be suitable for investors with a lower risk tolerance or for those prepared to take more risks in order to achieve greater profits.

However, the wheel strategy is essentially a range trade where the aim is to sell puts close to a local low and sell calls close to a local high. Knowing this, we can look for other strategies with different risk profiles that are used to express a directional view.

Here are two alternatives:

Option Collar (Mildly bullish, low-risk)

Here an investor buys the underlying asset and, at the same time buys a protective out-of-the-money put option and sells an out-of-the-money covered call. It may look something like this:

Buy one BTC at $20,000.

Buy one BTC $18,000 put option with 40 DTE and pay an $800 premium.

Sell one BTC $25,000 call option with 40 DTE and receive a $300 premium.

Cost - a net debit of $500 (Premium Paid - Premium Received)

Max upside of $4,500 ($25,000 - $20,000 - $500 Net Debit) -Assuming the investor sells the underlying at the expiration date.

Max Downside of $2,500 ($20,000 - $18,000 - $500 Net Debit) - Underlying sold at the expiration date.

Risk-Reversal (Bullish, high-risk)

An investor sells an out-of-the-money put option - using the premium to finance the purchase of an out-of-the-money call option.

For instance:

Sell one BTC $18,000 put option with 40 DTE and receive an $800 premium.

Buy one BTC $22,000 call option with 40 DTE and pay an $800 premium.

Cost $0 (Premium Paid - Premium Received).

In this example, the investor neither makes nor loses money if the option expires between $18,000 and $22,000, has unlimited upside potential above $22,000, and significant downside potential below $18,000.

Conclusion

The options wheel strategy is an advanced options play that is best suited to experienced investors with a solid knowledge of the options market. Though this particular strategy may be too technical for less-experienced options traders, the beauty of the options market is that there is something for everyone. Whether your view is bullish, bearish, or even neutral, you can profit using options at a risk level that suits your financial situation.

To learn more about how options can improve your trading, do check out our guides to various strategies. From the collar options strategy to the iron condor.